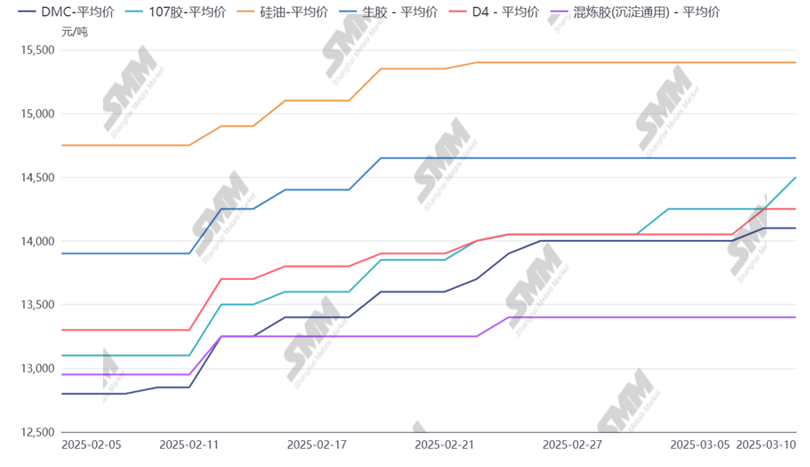

SMM March 10 News: Recently, the mainstream trading center of DMC has temporarily remained stable, with slight upward adjustments in low market prices. The silicone market's DMC prices have stayed stable for nearly two weeks since the last price increase. However, monomer enterprises' joint efforts to refrain from price cuts remain firm, and the 14,000 yuan/mt threshold for DMC has not yet been satisfied. There are plans for another slight price increase, and the market is showing a sentiment of price hikes.

Figure Price Trend of Silicone Products

Specifically, since the DMC price increase at the end of February, downstream willingness to purchase has been low, leading to increased pressure on some monomer enterprises to sell, with inventory showing an accumulation trend. However, downstream enterprises' raw material inventories are also about to be depleted. The overall market is in a stalemate, with prices temporarily stable. With the upcoming Adhesive Exhibition and the increased sentiment to stand firm on quotes among monomer enterprises, trading volume is expected to recover soon. Monomer enterprises also plan to raise prices in the near term. The basis for the price increase lies in the fact that domestic monomer production remains at a low level. Although some production lines have resumed recently, there are still many plans for reduced operating rates in the future. The overall industry is operating at around 70%, with limited supply pressure.

Regarding the forecast for DMC prices, as downstream demand is expected to enter the market soon, coupled with the low operating rates of monomer production, SMM expects a slight upward trend in the near term. The current round of price increases is estimated to be around 300 yuan/mt.

![Ferrous Metals May Continue Trading at Elevated Levels in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/yBlDX20251217171747.jpg)